It is over twenty years since Bill Gates famously said, “Banking is essential, banks are not”, and now it has started to happen — traditional banking in the US could very soon lose $11 billion to alternative finance every year according to Goldman Sachs.

Many old banks want a piece of the alternative finance growth they face build versus buy dilemma. For investors, the simple fact that the old industry is getting interested in alternative finance shows the disruptive influence the nascent sector has had already, and confirms that the financial services sector is ready for a reshape.

Big Banks Buy Into Alternative Finance

The past two years have seen traditional banks increasingly buying into alternative finance platforms, seeking for additional service and revenue streams. This global phenomenon has seen Barclays invest in Rainfin in South Africa, Australia’s Westpac invest in Society One, and in the UK, Santander announced as early as 2013 that they would be working in partnership with Funding Circle. In the US, banks have been agreeing partnerships with peer lenders such as Prosper and Lending Club, and investing heavily also in financial technologies, with Capital One buying personal finance tracking app Level Money earlier in the year.

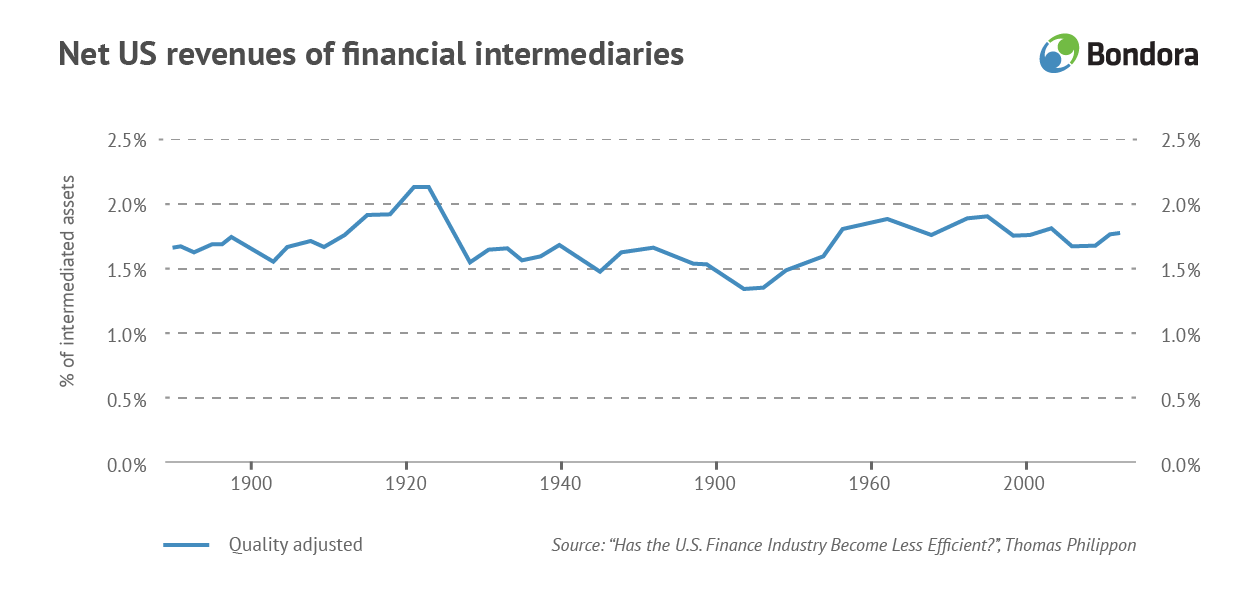

The stakes are high – the traditional financial services sector had been remarkably untouched by technological innovations, the relative unit cost of intermediation at traditional banks has not changed since 1900.

Alternative finance is a real disruptor in the cost side. Established platforms like the UK’s Lending Club are 60% more efficient than traditional banking, and as the sector grows and efficiencies of scale allow for even greater productivity and leaner models, there will come a tipping point after which the inefficiencies inherent in traditional banking may prove its undoing. With bull case estimates seeing alternative finance accounting for over 50% of SME and consumer finance in the UK and US by 2024, banks are worried.

Goldman Building

Financial institutions may be rethinking their approach, but not all major institutions are investing in existing alternative finance platforms. The entry into the market of Goldman Sachs in 2015 with its own consumer loan venture is especially interesting as they are establishing their own competitor to these platforms – a traditional financial institution looking to disrupt the disruptors (to quote industry insider Huy Nguyen Trieu).

Goldman Sachs has hedged its bets and come down on both sides of the ‚build versus buy‘ option, also investing in many fintech companies, and also in bigger picture rush of traditional banks into new alternative platforms is likely to be held back by the fact that this would undercut their other consumer lending activities such as unsecured loans or credit cards.

However, for investors in alternative finance, the market entry of Goldman Sachs may be the ultimate assurance that the traditional – and inefficient – model of banking is unsustainable. Under challenge from alternative finance innovators and progressive private businesses and institutions, the market is ripe for reshaping, and early investors will reap the benefits.