KEY TAKEAWAYS

- All the countries where we currently perform lending activities (Spain, Finland, Estonia) are now profitable

- All our country-grade segments (other than 3) have produced returns in line or above the expected return

- Net yields on Bondora are highest in the marketplace lending industry

- 98% of the portfolio above target return and returns in high teens across all countries

The history of Bondora Rating

Prior to 2015

Investors invested into loans across all countries based on the data and filters that were available on Bondora. There was neither risk-based pricing nor risk estimates from Bondora – basically investors had to decide themselves which loans seemed to have a good risk-return.

January 2015

Risk-based pricing was introduced for Bondora loans a.k.a. 1st generation of Bondora Rating.

December 3rd 2015

2nd generation of Bondora Rating and risk-based pricing was introduced.

Bondora Rating helps you make better investment decisions

We introduced our credit scoring and pricing model called Bondora Rating in January 2015. In short – it’s a set of data that in combination provides a more predictable risk-adjusted return.

There are two objectives for Bondora Rating:

- We want to facilitate loans with fair prices for borrowers, considering their individual risk profiles.

- We want to deliver reasonable returns for the investors, taking into account credit risk, country risk, cost of capital and market liquidity conditions.

Overall Bondora Rating helps package all the different risk-return variables into a single number – the interest rate – making investments across different territories and segments a seamless process.

What makes Bondora Rating unique?

“Bondora Rating and unique pricing algorithm enable us to score and price loan applications from different euro area markets on like-for-like basis, taking into account both borrower risk characteristics and country risk.” Bondora Credit Modelling Team

Introduction of Bondora Rating has had a strong positive effect on returns

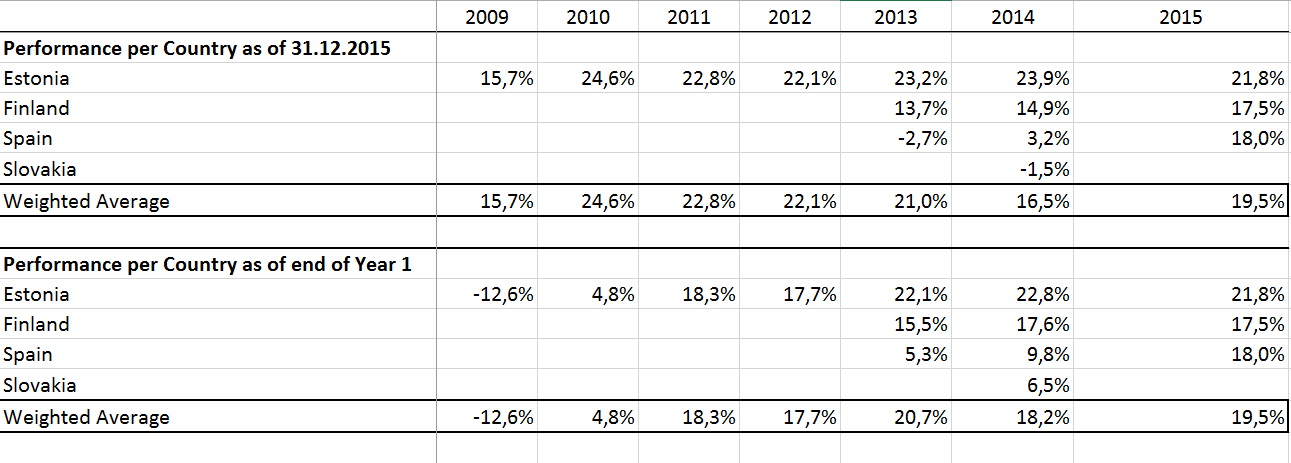

Performance by country

After Bondora Rating was implemented in 2015 the returns in new markets (Finland and Spain) have increased considerably. Spanish market that was at break-even level prior to Bondora Rating is now delivering net returns in high teens. These improvements will further strengthen Bondora’s position as one of the highest returning platforms in the marketplace lending industry (see Liberum Capital presentation page 10).

Figure 1. Performance of loan cohorts originated within the specific year as of 31.12.2015

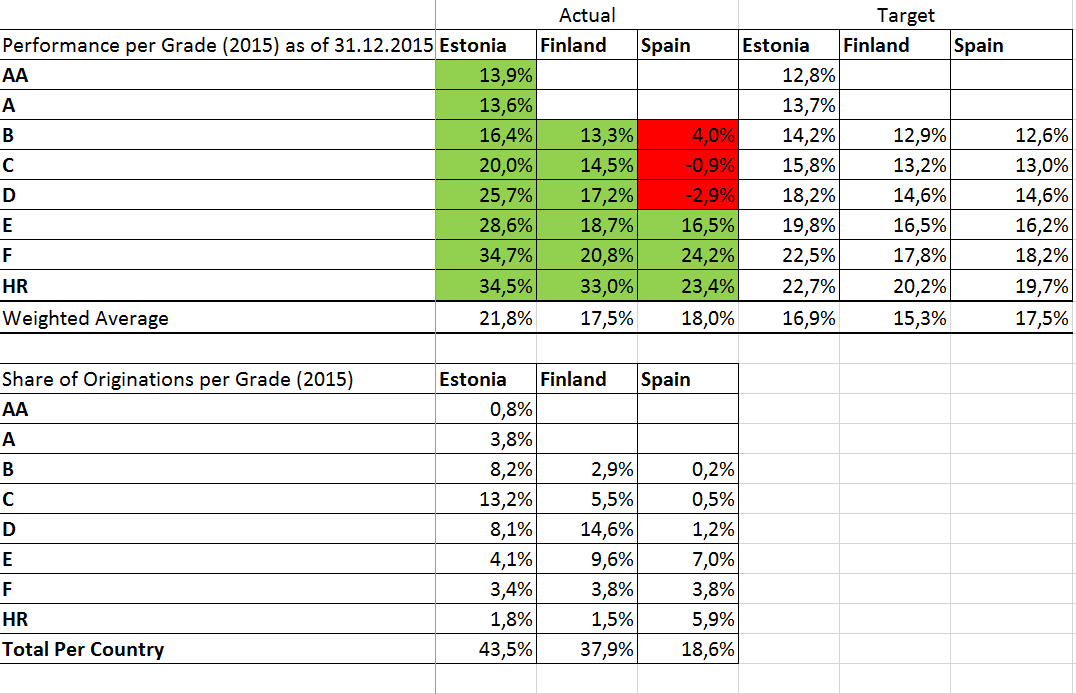

Performance by grade

Performance by grade

98.1% of the loans originated in 2015 have delivered net returns above or in-line with expectations. Only three grades performed below targets (Spanish B, C and D grades) however in total these made up 1.9% of the originations in 2015.

Figure 2. Performance of 2015 loans per country and Bondora Rating grade as of 31.12.2015

2nd generation models are built on significantly more data and hence are even more reliable

The 1st generation models delivered a significant improvement to the performance and predictability of loans originated on Bondora. However due to the relatively small sample sizes available in 2014 we witnessed performance variances between countries and grades. Therefore in order to address these limitations we released our 2nd generation models in December.

The main difference between the 1st and 2nd generation risk model is the underlying volume of historic data on which the models were built upon. The 2nd generation takes into account more parameters to estimate the probability of default of the specific customer even better.

2nd generation models for Spain and Finland were built on 10 times more data than for the 1st generation model and in Estonia we had two times more data. In effect the 2nd generation models for Spain and Finland were built on more data points than the 1st generation model in Estonia.

In addition the pricing models were adjusted to reflect changes in three other components that determine the risk-based price. Country risk factors were updated for the new macro-financial data. Risk-free rate of return was updated to reflect the current monetary conditions. Parameters of market rates of return were updated for the newly available data.

Our analysts are continuously working on finding new patterns to further improve the accuracy of the scoring and pricing systems. This is an ongoing process and remains core to what Bondora is doing.

NOW LET´S GET TECHNICAL

How are net returns calculated on Bondora?

We use the XIRR function (extended internal rate of return) to calculate the net return. XIRR is used to return the internal rate of return for a schedule of cash flows that are neither necessarily periodic (payments are not made on a single day each month) nor always positive (portfolio has both outgoing and incoming payments).

Internal rate of return is a discount rate that makes the net present value (NPV) of all cash flows (repayments minus initial investment) from a particular portfolio equal to zero. Discounting cash flow means that you are reducing the future cash flow projections to arrive at its present value (how much 100 euro in a year from now is worth today). This is mathematically done by dividing the future cash flow by 1 plus internal rate of return in the power of the fractional period (e.g. if you are using an annual internal rate of return and a payment is 4 months from now then you would take 1 plus internal rate of return to the power of 4/12).

XIRR uses the loan issue date and amount, loan actual repayment dates and amounts and sum of scheduled future principal repayments (this is assumed by us to equal the present value of the portfolio) to calculate the internal rate of return of your investment portfolio on Bondora. This approach writes off all overdue and unpaid principal and interest payments immediately from the calculation. No assumptions for future interest payments or loss provisions are made as this is expected to be covered within our approach to arriving at the present value of the portfolio.

In other words, if you would borrow money at a rate equal to the net return shown on Bondora in order to finance your investments you would end up break-even. If you are borrowing money at a lower rate or your alternative investment opportunities (e.g. mutual fund) have a lower rate of return than you are making a profit compared to other options and it makes sense to continue or increase investment.

Can net returns of an outstanding portfolio change over time?

Yes, your net return over time can fluctuate based on the actual interest and principal repayments received. Overdue loans might start performing again and current ones become delayed. Recovery processes can take years to collect every penny owed, so even performance of very old portfolios might increase substantially over the years. Over time our servicing, collection and recovery practices are continuously improved and even higher risk portfolios can start behaving like lower risk ones.

Most of the fluctuations (calculated as the current net return vs. the net return calculated in the end of the specific calendar year) we have witnessed have been positive due to recovery efforts. Using data since 2012 there have been variances between -8.1% to +4.4%.

Figure 3. Performance per country

Can the net return calculation be improved?

Theoretically it would be possible to substitute the current present value sum of scheduled future principal repayments with the sum of actual discounted future cash-flows. However in order to accomplish this you would need to make a significant amount of assumptions about the timing and amount of the future cash flows from your outstanding portfolio. You would need to estimate when and how much would current loans repay and you would have to make the same assumption also for delinquent loans. Furthermore, you would need to discount these cash flows with a rate equal to actual XIRR of the fully matured investment or use future dates and payment amounts granularly in the model . In the end, one would simply arrive at a number based on a lot of assumptions that still needs to be tested in reality.

We have seen some investors build their own risk-adjusted models that simply take the outstanding principal balance and reduce this by a fraction of the overdue loans. Although this might at face-value seem like a reasonable step, it ignores the fact that outstanding loans will make both interest and principal repayments, as will recovered loans. This logic could be applied to investments with very low rates of return (where future interest payments are discounted to zero or to negative numbers) however not to consumer loans carrying reasonable risk-adjusted interest rates. In other words in case one would discount overdue loans at the same time performing loans would be taken into the present value with a premium.

In case you are interested in trying to establish a better model for calculating the present value then we recommend using the Historic payments and Future cash flows data exports under public or your personal data. Simply using outstanding amounts is not sufficient for building a model.

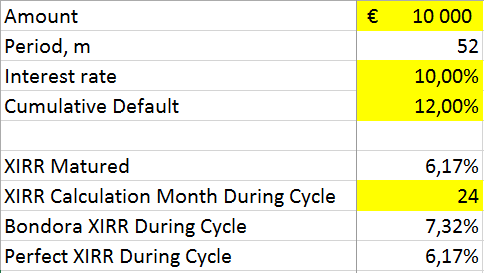

The enclosed file gives you a template example of discounting future cash flows and calculating XIRR at different points in time over the cycle of a portfolio. It also includes all the data used in the actual return calculations presented in the analyses above. Sheet ‘Xirr Calculator Example’ displays a basic model that includes some elements to include in your own analyses. Cells in yellow can be edited and white cells are fixed (please note that this example is for a 52 month term portfolio). Calculations related to ‘Bondora XIRR’ are based on the logic currently used on Bondora whilst ‘Perfect XIRR’ calculations are based on a situation where one would have perfect information available at any time during the cycle.

Figure 4. Bondora XIRR calculation model

Can net returns be positive even in case default rate is above the interest rate?

Net returns on a portfolio can be substantial even if cumulative default rate is equal or even above the nominal interest rate. This is because the performing portfolio continues to generate interest and repayments over the full cycle of the loan not only in a single year.

Over an average 52 month cycle the performing loans and parts of the non-performing loans generate and pay interest for 52 months. Therefore in case one would want to compare this number with the cumulative default rate then the nominal rate should either be cumulated as well or the default rate annualized over the 52 month period. In the calculation model shared above we have built cash flows for an imaginative portfolio with 10% nominal interest rate and a 12% cumulative default rate to illustrate this.

We have seen some investors build analyses where portfolio returns have been calculated as interest rate less cumulative default rate (or cumulative expected loss). Furthermore some of these analysis have been done by calculating tax income on the nominal interest rate although non-performing loans do not pay interest and hence are not taxed. Such models unfortunately are misleading at best due to the reasons explained above.

Please make sure you use the full cash flows when building your own portfolio evaluation models and apply taxation only to actual paid interest not nominal values.

*Correction: Amount lent per country figures were updated in the enclosed file to use the same definition for an issued loan as in the cash flow calculations, share of originations per grade and general statistics on Bondora website. This change slightly affected Weighted Average results, most notably net return of 2013 originations decreased by 0.1 per cent to 21.0% and net return for 2014 originations increased by 0.4 per cent to 16.5%.