We have great news for you this week – with excitement we are introducing our new dashboard and automated investment tool. Over the years Bondora has consistently delivered industry leading double digit returns to investors. With this new chapter in our story we will continue working hard to make investing a joyful experience. “The new dashboard and Portfolio Manager both will provide retail investors ease of use and they will love the simplicity”, says Pärtel Tomberg, CEO of Bondora.

MORE SIMPLICITY

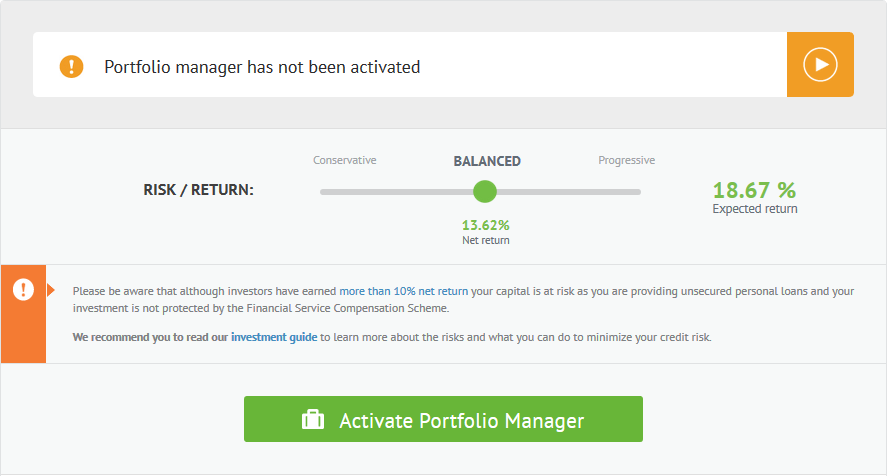

We have improved our Portfolio Manager with a simple interface where investing has been fully automated by our technology, leaving out unnecessary complexity. Automation helps you invest in more loans and thereby reduces the risks of some borrowers not repaying. „Our aim is to provide passive investors a high risk adjusted return with minimum amount of manual work“, notes Tomberg.

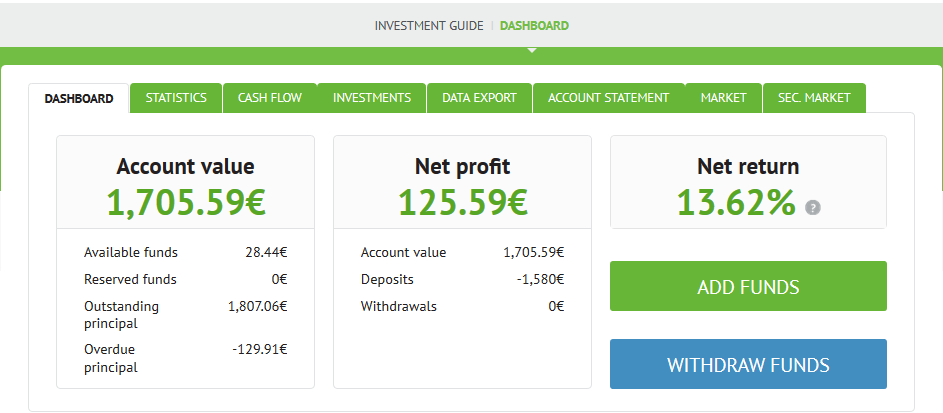

New dashboard is now a single control center to track and adjust your portfolio

The new dashboard will give you at a glance overview of your account leaving out the hunt for key data points across our web. We have updated dashboard statistics for value and profitability of your account. Additionally the deposit, withdrawal sections and Portfolio Manager have been combined into a single easy-to-use dashboard.

KEY BENEFITS

- You can immediately see the net profit of your portfolio on top of account value and net annualized return we were already showing

- You can add and withdraw funds from the dashboard

- You can immediately adjust your Portfolio Manager based on your investment/portfolio performance

New Portfolio Manager is now fully automated

NEW FEATURES

- Easy To Set Up

You can start investing in only two steps: first, select your desired target risk-return and second, agree to terms & conditions. The Portfolio Manager does the rest.

- Continuous Investment

Once you have set up the Portfolio Manager it will continue investing according to your chosen risk-return without you having to reactivate it at any point in time. You still have the chance to pause it at any point of time.

- Automatic Risk Balancing

The Portfolio Manager will monitor the current risk-return of your portfolio and continuously correct future investment to match the level you have selected. E.g. it will target lower risk loans when your portfolio risk level is higher than the selected risk-return.

- Automatic Diversification

The Portfolio Manager will take into account your portfolio size and will adjust the size of each investment that provides an optimal diversification level. Larger portfolios will invest in larger amounts and smaller portfolios in lower amounts. Bid amount changes as your portfolio size changes.

Are you an active investor? We have not forgotten you!

In the upcoming releases we also plan to roll out Bondora API (Application Program Interface) that allows active investors have their own customized investment strategies and reporting. There are already multiple 3rd party tools available in the market, e.g. LendTower has already announced to support our API. But until the new Bondora API is out, continue like you have invested before – hand-picking loan applications from the primary and secondary market (tabs Market and Sec. Market accordingly).

NOW LET´S GET TECHNICAL

If you are interested how the new dashboard and Portfolio Manager work under the hood then go ahead – read further to understand all the details.

What is the logic behind new „Account Value“?

Account value adds together your cash balance, reserved amount and outstanding portfolio. We subtract overdue payments to arrive at the net account value. This is how much we think your account at Bondora is worth.

What is the logic behind “Net Profit”?

We calculate the Net Profit of your portfolio by adjusting the Account Value. We subtract deposits and any outstanding loans you have and add withdrawals. In case you have deposited 1,000 euro, have an outstanding loan of 50 euro, have withdrawn 200 and your account value is 1,200 euro then your Net Profit is 1,200+200-1,000-50=350 euro.

How does automatic risk balancing work?

Portfolio Manager continuously measures the risk-return of your portfolio by calculating its weighted average risk. This risk factor is compared to the risk-return target you have set through the product interface. This calculation is done before each investment decision to determine the types of loans that can be added to your portfolio. The technology only invests in portfolios of loans that help you reach your target risk-return. In all of these calculations preference is given over reducing the risks over increasing the returns. This means that higher risk loans are only added to your portfolio when your portfolio risk is lower than the target not when the returns are lower than your target.

How does automatic diversification work?

The new Portfolio Manager is truly a single control center for your portfolio. Our technology adjusts the size of each investment amount based on the number of unique borrowers in your portfolio. We do not discriminate based on how you made the investment – every borrower with a performing loan is included in the calculations. The system carefully increases the investment size as your active portfolio grows whilst making sure the risks do not increase. The investment size can also be adjusted downwards if the size of your portfolio starts decreasing.

The minimum bid size is 5 euro and maximum 80 euro. The bid size is doubled after each time your portfolio increases by 200 loans. 200 is an important number because analysis of the investors’ portfolios shows that the risks of a portfolio substantially decrease after reaching 200 unique loans. This means that your portfolio return becomes stable and on 95% of cases is above 10% of return. Therefore increasing the size of the investments after each 200 new loans allows you to lend your money faster without increasing risks.

How are investments placed on the market?

Portfolio Managers invest into new loan applications periodically throughout the day. The preference between different investors is set so that each investor on average has the same waiting time to invest all of their available capital providing for a very fair marketplace.

The Portfolio Manager analyses your current portfolio, your available capital and all loans available on the market and invests in a sub-set of loans that help you reach your risk-return target fastest. Lower risk loans are always preferred over higher risk loans. In the future the Portfolio Manager will also start selling and buying loans on the Secondary Market. You will then have a single interface for building up or exiting from your portfolio making the experience truly great.

What if I already have loans with Bondora?

Our technology automatically reserves an amount equal to your loan repayments due over the next 60 day period. Therefore you do not have to worry that the Portfolio Manager will use the money you have saved for making repayments.