Welcome to October’s Secondary Market statistics blog post. Recently, we talked about the most common methods used to purchase current, overdue and defaulted P2P loans and whether these transactions were made at a premium, discounted or par value.

Below, we are going to do the same based on the transactions made in September.

Total volume

In September 2018, the total amount of investments made through the Secondary Market totaled €1,054,514, an increase of approximately 15.1% (+€138,736) compared to August. Similar to last month, the manual investing option led the way in volume – ahead of Portfolio Manager and the API for the fourth time.

In September, the total amount of manual investments increased by over 37% (+€149,421) and the share in relation to the total stands at 52.2%. In comparison, the amount of purchases made via the API on the Secondary Market decreased by 14.6% (-€23,162) and the total share for the month decreased to 12.8%. Along with the changes to the API and manual options, Portfolio Manager saw a small increase of 3.5% and held approximately 35% of the total share.

For information on our overall funding statistics, read more here.

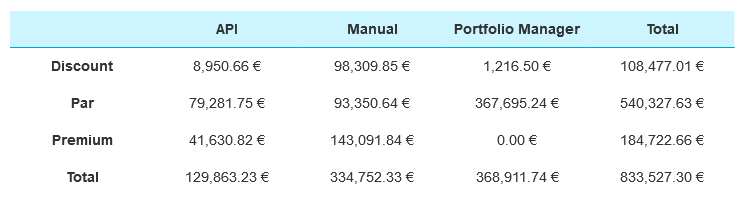

Current loans

In line with previous months, Portfolio Manager still leads the way in purchasing current loans at a par value. On the other hand, manual investors were the most successful at purchasing current loans at a discounted value (€98,310). In addition to this, manual investors purchased €143,092 of current loans at a premium, compared to €41,631 via the API.

No priority is given to any investment method (including Portfolio Manager) and there’s no bias based on an investor’s portfolio size.

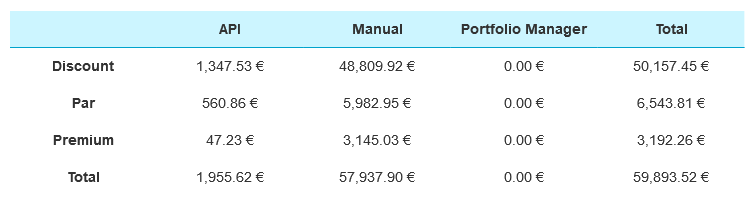

Overdue loans

In September, there was an increase of 100.5% in the total amount of overdue P2P loans purchased through the Secondary Market. The majority of these transactions were completed manually and at a discount (€48,810).

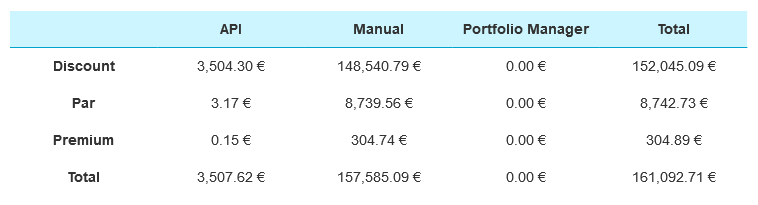

Defaulted loans

Overall, the total amount of defaulted loans purchased through the Secondary Market increased by 44.6% in September. The most notable change here is the volume of the amount purchased manually and at a discount (€148,541).

In comparison, only €0.15 of defaulted loans were purchased at a premium via the API. A unique strategy used by a small number of investors is to purchase defaulted loans with a significant discount with the plan to reap the rewards once the collection and recovery process begins to generate a cash flow. However, it should be noted that this is an extremely high risk strategy that often results in a poor net return and even losses.

Good to know

Selling your loans can result in a loss of the original principal, as the Secondary Market typically does not provide a high enough premium for current loans to compensate for the non-performing part of the portfolio. Therefore, we advise to proceed with caution and not to try and sell everything at once if you see a percentage of your portfolio in default. It is likely that you will quickly sell the performing part of your portfolio and be left with the loans in recovery, significantly damaging your expected return.

The speed of the sales process depends on the market demand. In general, current loans are more liquid and will usually be sold within a day if sold at par value or a slight premium. Delinquent loans may take more time or the sale can be unsuccessful. As soon as another investor has purchased your loan, you will receive the funds directly to your Bondora account.

If you’re still unsure how to sell your loans, you should always get in touch on investor@bondora.com and have a chat with one of our experienced Investor Relations Associates who will walk you through it step by step.