Who am I?

My name is Lars Wrobbel and I am the founder of the biggest German P2P lending blog Passives Einkommen mit P2P. I have been posting about my investments in P2P loans since 2015 and have already gathered experience on over 20 P2P platforms, 15 of which are still active investments in my portfolio. I was also the initiator for the P2P-Conference, together with my business partner and friend, Kolja Barghoorn from AktienMitKopf. The first conference, which took place in the Baltic States last year, was held around the topic of P2P loans. Together, we also wrote Germany’s most famous book on the topic (which is also available in English). If you want to know more about me, please read my About Me page or join our Community with almost 10,000 investors.

Bondora is my biggest investment in P2P loans, but my investments are primarily focused on the stock market. This not because I trust P2P loans less, but simply because I have a longer investment history with the stock market.

Where we find ourselves today

The COVID-19 crisis is the second real financial crisis that I have experienced as an investor; the first being the 2008/2009 financial crisis. And just like back then, it hit with a severity that many would have thought unimaginable. While in 2008/2009 I was still a very inexperienced investor who had to struggle with the situation, I have learnt a lot over the last 12 years. At least, I hope so 🙂

Today we are in the second half of May and the crash on the stock market happened more than 2 months ago. COVID-19 is beginning to flatten out in most countries in the world and the lockdowns, which caused us so much trouble, are gradually being relaxed and lifted. However, at the moment it is still uncertain whether this was the end or whether we have to expect further and far more violent waves of the virus. In the economy, however, it is certain that this will not be the end. We will have to deal with the consequences of the lockdowns for a long time to come.

With this article I would like to give you a brief insight into my investments, my strategy, and my behavior in the crisis situation, and what has happened in my portfolio since then. This should serve as a small guideline, and also as a motivator for you not to make hasty decisions. You should also question frightening YouTube videos and news. Rather read some good books and take it easy in order to properly position and prepare yourself for the future.

My investments

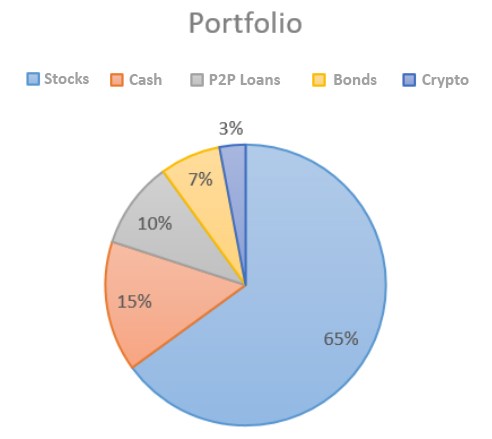

My portfolio is divided into several different asset classes, which I would like to show you here. The portfolio has grown over my years as an investor and therefore should be based on the presented basic values. But of course, in times like these, the allocation is very dynamic. The most exciting components for me are, at the moment, undoubtedly the P2P loans and cryptocurrencies.

- Stock market approx. 65%

- 50% individual dividend stocks of solid market giants

- 25% global ETFs (commodities included)

- 25% US, Canadian, British and Australian REITs

- Cash approx. 15%

- 75% usable within 3-6 months

- 25% immediately available via overnight deposits

- P2P loans approx. 10%

- Distributed across about 15 active P2P platforms

- Bonds approx. 7%

- 90% top-rated government bonds

- 10% US municipal bonds

- Cryptocurrencies

approx. 3%

- Mainly Bitcoin & Ethereum

My strategy

Over the last few years, and especially through my involvement in the P2P loans 2014, I have come to realize that investments, which generate constant cash flow, are what motivates me the most. Over time, they have become an increasingly important pillar of support that I can rely on when in doubt.

About 10-15% of my income comes from the various payments of my investments and I could (if I had to) live off it without any problems. However, 99% of the payments generated in my lifetime have, so far, been reinvested 1:1 in the respective investments. However, due to the funds that are released almost daily, you can shift your portfolio very dynamically, and quickly, without having to reinvest your own funds.

P2P loans are designed for generating cash flow. With other investments, like cryptocurrencies for example, it gets harder. But even with crypto there are already solutions that can be used to generate cash flow that hardly need to hide behind the returns of P2P platforms. Even with bonds, it is possible to use financial tools that allow you to make ongoing payments.

My portfolio during the crisis

In March, the very thing that the majority of investors feared, came to pass. The market collapsed, horrendous reports went around the world and every industry seemed to be affected by the problems. A bull market that had lasted for more than a decade ended with a bang. Investors left the various asset classes in droves.

P2P loans seemed to be particularly affected due to the young age of the industry. Fueled by market criers on the World Wide Web who were already predicting the end of the P2P industry, the ‘bank run’ began and, as we now know, a few platforms went under. Maybe more will follow. YouTubers who advertised P2P platforms a week before now warned against investing, stopped their own investments and cashed out their money.

From my experience, however, I recognized this situation and therefore did exactly what I always do when the financial world turns upside down: At first, nothing at all, and then I continue to do nothing 🙂 My strategy has been established and has stood fast for years — I didn’t develop it to throw it overboard during a crisis. Quick decisions are usually bad decisions.

After the first few days, I took the first opportunity to put the readily available cash portion of my portfolio into the stock market. After that I continued to concentrate the available cash flow mainly on the stock market and also on the crypto market, as this was also hit very hard by the market crash. In addition, the Bitcoin Halving was another exciting moment to look forward to.

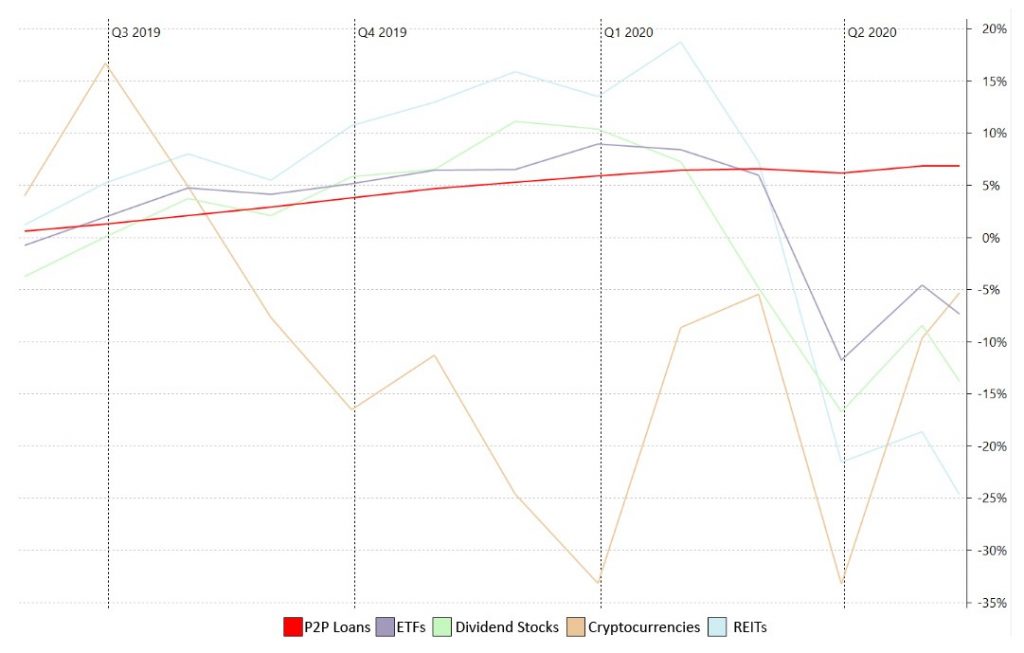

In contrast, I left the P2P loans untouched. And indeed, this asset class turned out to be the most stable so far, which is nicely illustrated by this chart from the Portfolio Performance Software.

The behavior of most P2P platforms strengthened my opinion that this crisis can also be a great opportunity for the industry. In contrast to many other industries, the communication was investor-oriented and people adjusted to the new situation very quickly.

My summary and roadmap for the rest of the year

In the end, it’s business as usual. Ultimately, it pays off not to leave your strategy once it has been defined, and to take advantage of any opportunities that arise. That is exactly how I will continue with my investments. I will also increase the immediately available cash portion of my portfolio, in case there’s another market crash in the coming months.

As for my P2P investment: All my active P2P positions are held and the strategy is being pursued. The P2P loans have proven to be the most stable of all my asset classes over the last 2 months and thus there will also be a selective build-up of platforms.

This crash is also extremely important for the P2P industry. It ensured that the weaker platforms were thrown out of the market, and that only the strong will survive.

In conclusion: Stay true to your strategy and do not make any rash decisions! If you are interested in my reports, please visit my Blog. I look forward to seeing you there!

The views and opinions expressed in this article are those of the guest blogger and do not necessarily reflect the official policy or position of Bondora.