Even though originations and investments declined somewhat in September, it remained an exciting month for us. We launched our loan product in the Netherlands, and Spanish loan originations exceeded €1M for the first time since March 2020. Read more:

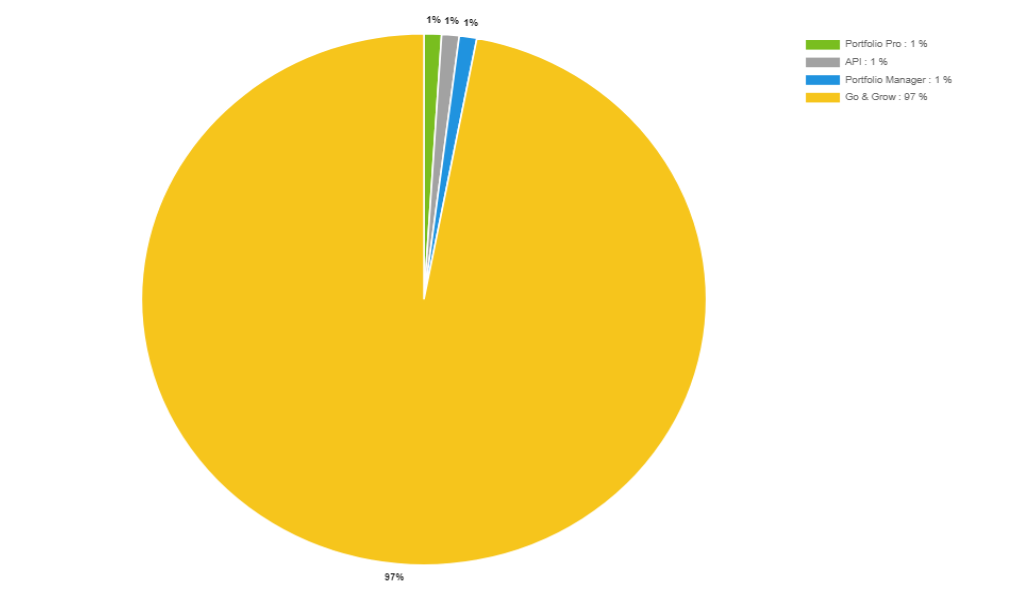

Investment by product

In September, investments totaled €12,252,773. This is a 14.8% drop from August. This waning was mostly due to a large decline in Go & Grow investments, but the other product categories also experienced lower activity, as shown here:

Go & Grow – 14.8%

Portfolio Manager – 1.8%

Portfolio Pro – 1.3%

API – 20.1%

Once again, Go & Grow’s figures had the most significant effect, as it is the most used investment product, making up 96.9% of all investments. It received €11,876,545 in investments. Portfolio Manager received €219,578 and Portfolio Pro €155,355. The API accounts for the remaining €1,295.

Loan originations

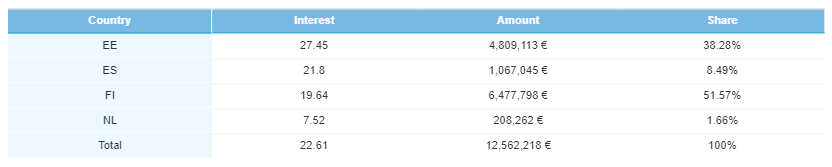

Overall, our loan origination figures declined by 12.8% to €12,562,218. This decline was due to drops in Estonian and Finnish originations. Nonetheless, September was an excellent month for our loan markets, in general.

First, we launched the Netherlands market in September and have already originated over €200,000 worth of loans! And in Spain, we originated over €1M worth of loans in September. This is the first time we broke the €1M milestone since relaunching the Spanish market in September 2021.

Country breakdown

Unsurprisingly, Spain had the most noticeable growth, increasing by a mammoth 126.2% to €1,067,045 loan originations.

On the other end of the spectrum, the largest decline came from Finland, dropping by 21.8%. Finland also still has the majority of originations, 51.6%, which equals €6,477,798’s worth of loans.

Estonia’s share declined by 14.9%, totaling a 38.3% share of €4,809,113’s worth of loans.

The average interest rate increased from 22.3% to 22.8%. Once again, the average Spanish interest rate remained the same at 21.8%. Estonia’s average interest rate increased again from 26.2% to 27.5%. In Finland, it remained stable at 19.6%. And the first-ever interest rate for the Dutch market is 7.5%.

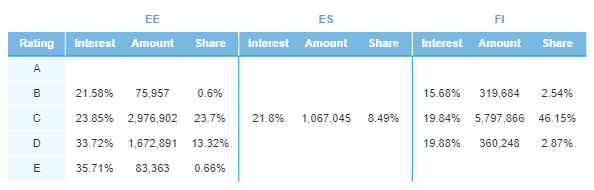

As always, C-rated loans are the most populated risk-rating category in all our markets. Estonia’s C-rated share decreased slightly from 24.9% to 23.7%. It also decreased slightly in Finland—from 51.7% to 46.2%. We only originate C-rated loans in Spain, making up 8.5% of the entire loan portfolio. This is an impressive jump from August’s 3.3%.

In Estonia, the D/rated loan category increased from 10.9% to 13.3%. Once again, the B-rated category was subject to change, nearly disappearing from a 2.5% total share in August to 0.6% in September.

In Finland, the B-rated category remained more or less the same, but the D-rated category decreased from 3.1% to 2.9%.

Exciting times for loan markets

Investments declined for a second month, but we are still happy with the performance. And despite declines across our Finnish and Estonian loan markets, the Spanish market’s continued growth and the Dutch market’s launch excite us for the future. If the current origination rate of the Netherlands market is anything to go by, we are in for an exciting last quarter of 2022.

Want to see more detailed information? Head to our public statistics page for the most up-to-date stats!