In November 2014 we introduced Bondora Ratings with the goal of pricing loans in accordance with the individual risk associated with a particular borrower. Thus, the interest rate at origination is based on the Expected Loss (EL) associated with a particular Rating and the Expected Return E(R) (or I = EL% + E(R) if presented as a simplified formula). As the interest rate is set at the moment of loan origination and cannot be changed during the loan lifespan, correctly forecasting the Expected Loss (which is the default less the recovery) is critical for ensuring the return expected by the investors.

It’s been six months since we introduced Bondora Ratings (and slightly less since we started pricing loans based on Bondora Ratings), so we decided it’s a good time to take a look at the performance of different loan categories to see if the Expected Loss rates used in pricing are in line with the actual default levels. For the purposes of this analysis we used loans that were originated in 2014 (we calculated Bondora Ratings also for the loans issued prior to November 2014); thus, it should be noted that not all of the loans reached 12 months in maturity.

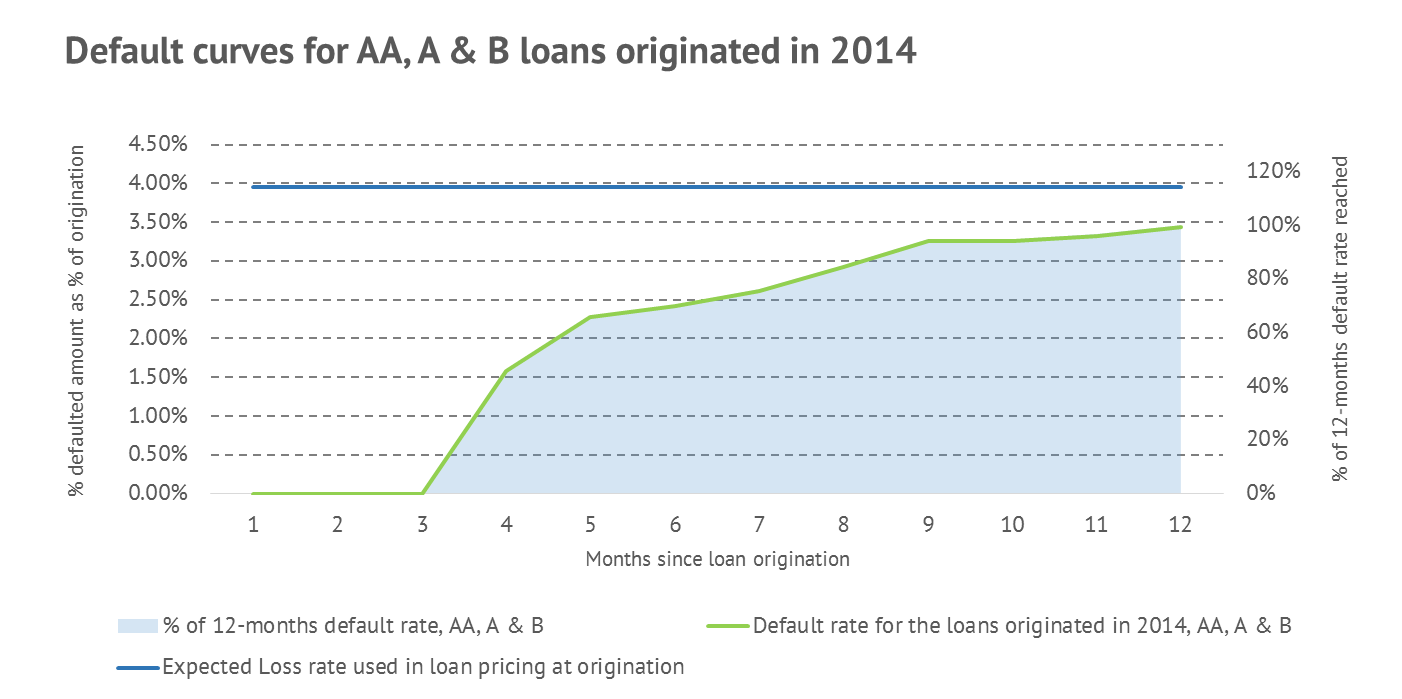

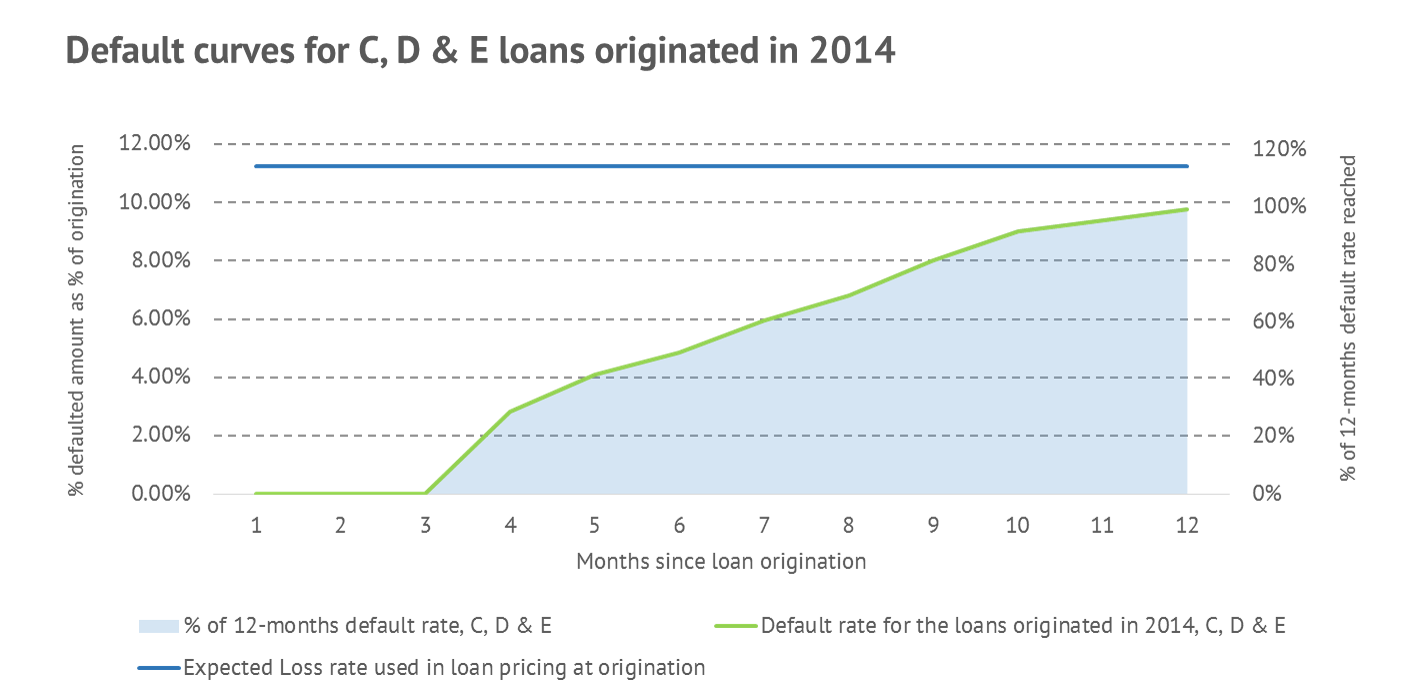

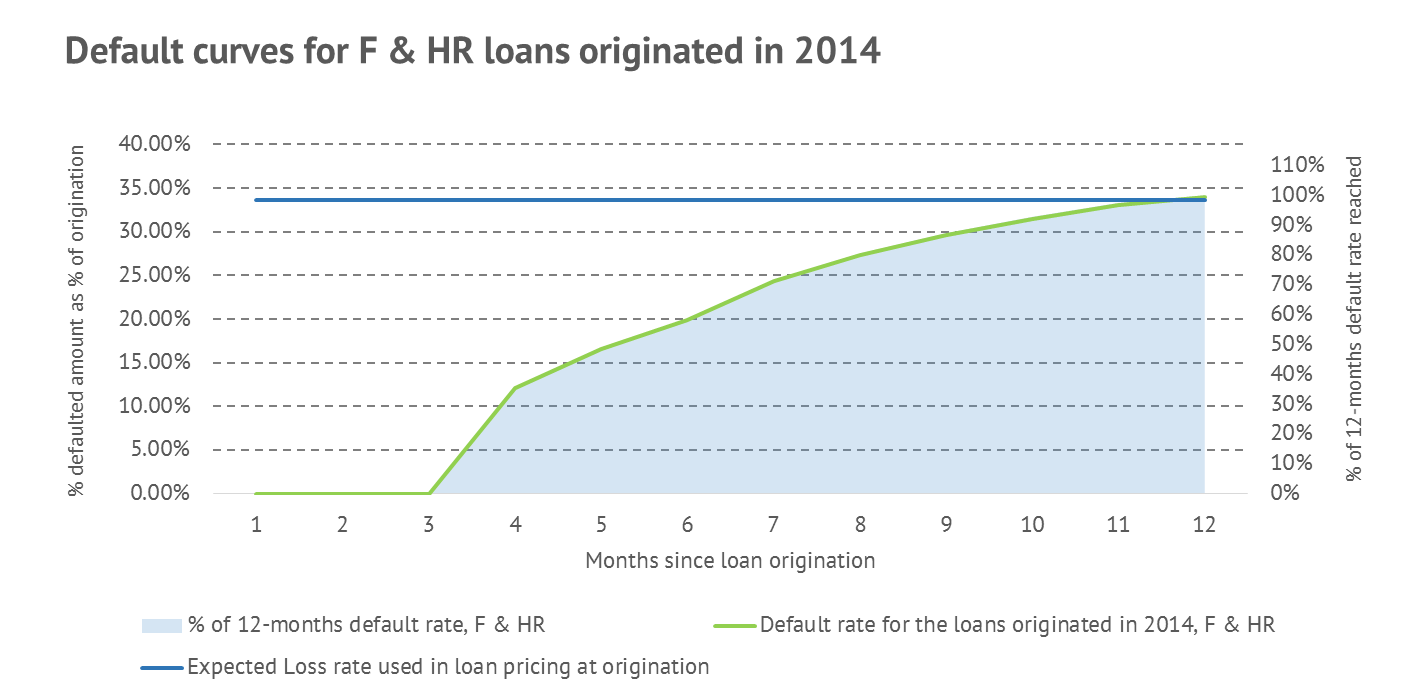

The below charts display the following metrics for different Rating groups (as of Quarter 1, 2015):

- ── Percentage of defaulted loans (by amount) by months since the origination (i.e. less than 2.5% of loans with AA, A and B Rating defaulted after 6 months since origination)

- ▄▄ Percentage of the 12-months default rate reached (i.e. the default rate after 12 months for the loans with AA, A and B Rating is 3.5% and by the 9th month since origination loans reach 95% of this level)

- ── Expected Loss rate used in loan pricing

Please note that the Default Rate represents the volume of defaulted loans before the recovery. Thus, the recovery for the defaulted loans will result in the Actual Loss rate being lower than the Default Rate shown on the charts above.

The chart above illustrates that the loans with the Ratings AA, A and B that were issued in 2014 so far are performing better than expected, as indicated by the actual default level being confidently below the Expected Loss rate.

Similarly to the loans with Ratings AA, A and B, the loans with the Ratings C, D and E that were issued in 2014 are performing better than expected, as indicated by the actual default level being below the Expected Loss rate.

The loans with Ratings F and HR are performance in line with the expectations and the recovery is expected to improve the performance of this loan category over time by decreasing the Actual Loss from the defaulted loans.

We hope that this analysis will help you make better investment decisions and plan to revisit it after more 2014 loans reach 12 months maturity.

Photo credit: mamsoftware.com/en